How to Pay Off Your 30-year Mortgage in 7-10 Years

Decoding the 30-Year Mortgage: Why Banks Structure Home Loans to Maximise Interest and How You Can Pay Off Your Loan Sooner

I’ve been coming across videos lately that claim you can pay off your mortgage in record time, sometimes in as little as 7 years. But most of these videos don’t explain how it’s done until you’ve subscribed or signed up for something.

More often than not, there’s an investment company, finance firm, or real estate agent behind it all, hoping to sell you something. So, I wanted to find out how it works, understand the maths, and share it with you.

Let’s dive into the mechanics of how it’s done.

Before we dive in, I want to make something clear: I’m not a qualified financial adviser, nor am I allowed to give financial advice. This article is for information only, based on my research (while waiting for my car to be serviced).

Everyone’s financial situation differs, so it’s important to talk to a qualified financial adviser before making any financial decisions.

Why Banks Set Up Mortgages the Way They Do

Buying a home is one of the biggest financial decisions you’ll ever make, and for most of us, that means taking out a mortgage.

So why are mortgages typically structured as 30-year loans? Why do banks stretch out the repayment period, making it feel like you’ll be paying off your house forever?

The answer lies in how interest works and how banks profit from it.

When you take out a mortgage, you’re borrowing a significant sum of money, often hundreds of thousands of dollars. Banks charge you interest on that loan, which is essentially the cost of borrowing the money.

The longer you take to repay the loan, the more interest you’ll pay over time, which is where the bank makes its money.

In a typical 30-year mortgage, your monthly payment is calculated to cover both the interest and the principal (the amount you borrowed).

However, in the early years of your mortgage, much of your payment goes toward interest, with only a small amount reducing the principal. This is because banks use a process called amortisation to structure your payments.

Amortisation is a method where the loan is paid off in equal monthly instalments over a set period. But while your monthly payment stays the same, the breakdown of what goes to interest and what goes to principal changes.

At the beginning of your mortgage, the outstanding balance is high, so the interest portion is large, and the principal portion is (very) small. Over time, as the principal decreases, so does the interest, and more of your payment goes toward reducing the principal.

Let’s break this down with a simple example:

Imagine you’ve taken out a $500,000 mortgage at a 4% interest rate for 30 years. Your monthly payment would be around $2,387. In the first month, you’ll pay about $1,667 in interest and only $720 toward the principal.

It’s only after many years of payments that more of your money goes toward the principal rather than the interest.

The Maths Behind (Skip if you are not interested)

Let’s use an example of a $500,000 mortgage at a 4% interest rate for 30 years to see how the numbers work out.

Total Interest Paid Over 30 Years

Loan Amount: $500,000

Interest Rate: 4%

Loan Term: 30 years

Monthly Payment:

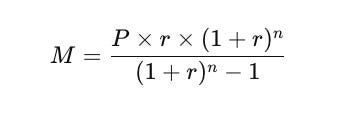

The monthly payment is calculated using the formula for a fixed-rate mortgage, which results in (from ChatGPT):

Where:

M = monthly payment

P = principal loan amount ($500,000)

r = monthly interest rate (4% annual interest rate / 12 months = 0.00333)

n = number of payments (30 years × 12 months = 360 payments)

Using this formula, the monthly payment would be approximately $2,387

Total Payments Over 30 Years:

$2,387 × 360 = $859,320

Total Interest Paid Over 30 Years: $859,320 (what you will pay) − $500,000 (what you borrowed) = $359,320 (Interest)

So, in this scenario, you end up paying $359,320 in interest over the 30 years.

Breakdown of First Payment

In the first payment of $2,387:

Interest: $500,000 × 0.00333 = $1,667

Principal: $2,387 − $1,667 = $720

As you can see, $1,667 of your first payment goes to interest, and only $720 goes towards reducing your principal.

Breakdown After 10 Years

After making payments for 10 years:

Remaining Balance: Approximately $396,000

Interest on Next Payment: $396,000 × 0.00333 = $1,318

Principal on Next Payment: $2,387 − $1,318 = $1,069

Now, $1,069 goes toward the principal, but the bank has already collected much of the total interest during those first 10 years.

By front-loading the interest, they collect most of their profit in the early years of the loan. If you sell your house or refinance before the loan term is up, the bank still walks away with a significant portion of the interest.

The longer the term of your loan, the more interest you’ll pay. That’s why a 30-year mortgage, while offering lower monthly payments, results in much higher total interest paid compared to a 15-year mortgage. It’s also why paying off your mortgage faster can save you a substantial amount of money.

What about interest-only mortgages?

Interest-only mortgages can be tempting because they offer lower monthly payments at the outset. However, they carry significant long-term risks, especially for borrowers who aren’t fully aware of the implications.

How Interest-Only Mortgages Work

In an interest-only mortgage, for a set period (typically 5 to 10 years), you pay only the interest on the loan, not any of the principal. This means your monthly payments are lower because you’re not paying down the loan balance. After the interest-only period ends, the loan typically converts to a traditional amortising mortgage, where you pay both principal and interest. Your payments increase because you’re now paying off the principal over a shorter remaining term.

The Risks of Interest-Only Mortgages

No Equity Built During Interest-Only Period

What It Means: Since you’re only paying interest during the initial period, you’re not building any equity in your home unless the property appreciates in value. If the housing market stagnates or declines, you could end up with little or no equity or even owe more than your home is worth.

Why It’s Bad: Without building equity, you’re not really “buying” your home; you’re just paying rent to the bank. This can leave you vulnerable if you need to sell or refinance.

Payment Shock When Interest-Only Period Ends

What It Means: After the interest-only period ends, your monthly payments will increase significantly because you’ll start paying off the principal. This can be a shock if you haven’t prepared for it.

Why It’s Bad: If your income hasn’t increased or if you haven’t saved enough to manage the higher payments, you could struggle to make ends meet, potentially leading to financial stress or even foreclosure.

Higher Total Interest Paid

What It Means: Because you’re not reducing the principal during the interest-only period, you end up paying more interest over the life of the loan. If you refinance or extend the loan term, you may end up paying even more in interest.

Why It’s Bad: While the initial payments are lower, the long-term cost of an interest-only mortgage can be much higher than a traditional mortgage, making it more expensive in the end.

Potential for Negative Amortisation

What It Means: If your interest-only mortgage has a feature that allows you to pay less than the interest due (such as with some adjustable-rate mortgages), the unpaid interest gets added to the principal, increasing the amount you owe.

Why It’s Bad: Negative amortisation can lead to owing more than you originally borrowed, which is a risky situation, especially if property values decline or your financial situation changes.

Who Might Consider an Interest-Only Mortgage?

Interest-only mortgages might be suitable for certain borrowers under specific circumstances:

Investors: Those who plan to sell the property before the interest-only period ends, potentially benefiting from property appreciation.

High Income Later: Borrowers who expect a significant increase in income soon and want lower payments now to manage cash flow.

Short-Term Ownership: If you’re buying a home you plan to sell within a few years, an interest-only mortgage might make sense as a short-term strategy.

Proceed with Caution

Interest-only mortgages can be risky, particularly for homeowners who aren’t prepared for the higher payments that kick in after the interest-only period. While they can offer short-term financial flexibility, they often lead to higher costs and increased financial risk over the long term. It’s crucial to consider your financial situation and long-term goals before choosing this type of mortgage. As always, consulting with a qualified financial adviser can help you determine whether an interest-only mortgage is a suitable option for you.

How to Pay Off Your Mortgage in 7-10 Years Instead of 30 Years

The good news is that you can take steps to pay it off much sooner—often in 7 to 10 years. It’s a strategy that many homeowners successfully implement by making extra payments, refinancing, or using creative approaches to manage their finances.

Make Biweekly Payments

One of the simplest ways to pay off your mortgage faster is to switch from monthly payments to biweekly payments. Here’s how it works:

Biweekly Payment Setup: Instead of making one monthly payment, you make half of your mortgage payment every two weeks. This results in 26 half-payments per year (13 full payments), rather than 12 full payments.

Impact on Loan Term: That extra payment goes directly toward your principal, reducing the amount of interest you’ll pay over time and shortening the life of your loan. Over the course of a 30-year mortgage, switching to biweekly payments could shave off about 4-6 years from your mortgage term.

Example:

Let’s say you have the same $500,000 mortgage at 4% interest. By making biweekly payments, you might reduce the term to around 25-26 years and save thousands of dollars in interest.

Make Extra Principal Payments

Another effective strategy is to make extra payments directly toward the principal.

Monthly Extra Payments: Add a fixed amount to your monthly payment that goes directly to the principal. Even an extra $100 per month can make a big difference.

Lump-Sum Payments: Whenever you receive a bonus, tax refund, or any other windfall, consider putting it toward your mortgage principal.

Round-Up Payments: Simply rounding up your mortgage payment to the nearest hundred can add up over time.

Example:

If you make an extra $200 monthly payment on that $500,000 mortgage, you could pay off the loan 6-7 years earlier and save tens of thousands of dollars in interest.

Refinance to a Shorter-Term Loan

Refinancing your mortgage to a shorter term, like 15 or 20 years, is another way to pay it off faster. While your monthly payments will be higher, you’ll pay significantly less interest over the life of the loan.

Lower Interest Rates: Shorter-term loans typically have lower interest rates, which means more of your payment goes toward reducing the principal from the start.

Faster Payoff: By refinancing to a 15-year loan, you’ll cut the time you spend paying off your mortgage in half and save a substantial amount of interest.

Example:

Refinancing that $500,000 mortgage from a 30-year term at 4% to a 15-year term at 3.5% would increase your monthly payment from $2,387 to about $3,570. However, you’d pay off the loan in half the time and save over $150,000 in interest.

Use the Debt Snowball or Avalanche Method

If you have multiple debts, including your mortgage, using the debt snowball or avalanche methods can help free up money to pay off your mortgage faster.

Debt Snowball Method: Focus on paying off your smallest debt first while making minimum payments on the others. Once the smallest debt is paid off, apply that payment to the next smallest debt, and so on. This frees up more money for your mortgage.

Debt Avalanche Method: Focus on paying off the debt with the highest interest rate first, then move on to the next highest. This method saves more money in interest, which you can then apply to your mortgage.

Example:

If you pay off a high-interest credit card, you could redirect that payment to your mortgage, accelerating your payoff.

Consider a Mortgage Acceleration Program

Some homeowners use mortgage acceleration programs to pay off their mortgage faster. These programs often involve using a home equity line of credit (HELOC), also known as an offset account, with your regular mortgage payments.

How It Works: You deposit all your income into a HELOC and use the HELOC to pay your mortgage. As you earn money and deposit it into the HELOC, you reduce the HELOC balance, which reduces your interest costs. This method can be complex and isn’t for everyone, but it can be an effective way to pay off your mortgage faster if managed correctly.

It also requires discipline not to withdraw your deposit for an expensive holiday when you can. This will immediately increase your interest payment even though your monthly payment remains the same. It is important to monitor interest payments with each monthly payment to keep track of the mortgage’s actual cost.

Live Below Your Means

The simplest, yet most effective, strategy is to live below your means and apply any extra savings to your mortgage. This requires discipline and budgeting, but the payoff can be huge.

Budgeting: Track your expenses, cut unnecessary spending, and redirect those savings to your mortgage.

Lifestyle Adjustments: Consider downsizing, reducing discretionary spending, or finding additional sources of income to speed up your mortgage payments. I wrote about this previously in the article “Living within your means.”

Conclusion

Paying off a 30-year mortgage in 7-10 years might seem like a daunting task, but it’s entirely possible with the right strategies and a bit of discipline.

By understanding how banks structure mortgages and taking steps to reduce your principal balance faster, you can save a substantial amount of money and achieve the financial freedom of owning your home outright much sooner.

Whether you choose to make biweekly payments, refinance, or adopt a more aggressive savings strategy, the key is to start now and stay consistent. Your future self will thank you!